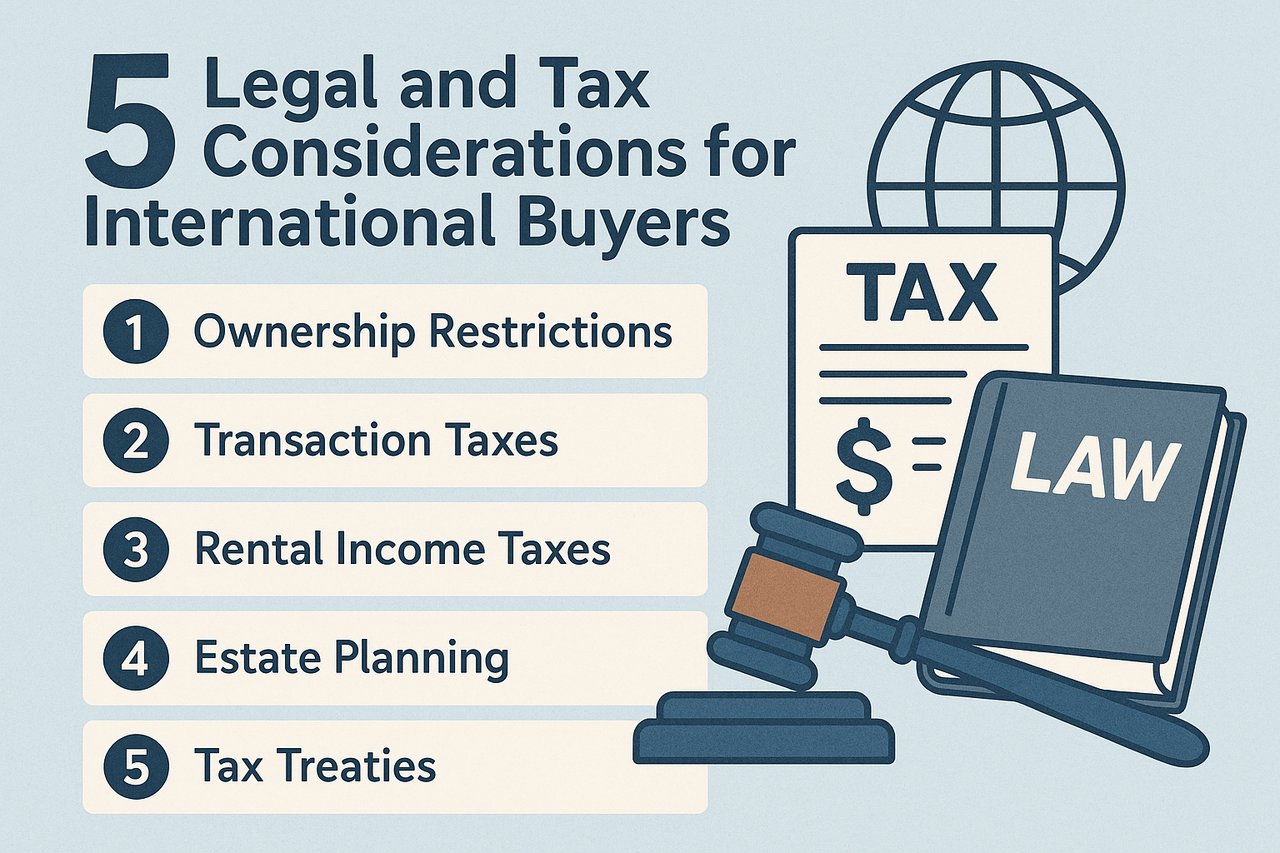

Investing in New York City real estate as an international buyer can be a lucrative and rewarding venture. But before signing a purchase agreement, it's essential to understand the complex web of U.S. legal requirements, tax exposure, and ownership options. Without proper planning, foreign investors may face unnecessary penalties, miss out on valuable deductions, or overlook important estate planning gaps.

This comprehensive guide outlines five of the most important legal and tax considerations non-resident buyers must understand before purchasing U.S. property ,especially in NYC.

1. Choosing the Right Ownership Structure

The way you hold title to your property in the United States impacts privacy, taxation, asset protection, and your heirs' ability to inherit the property. International buyers have several options, each with its own benefits and drawbacks.

Personal Ownership (Title in Your Name)

This is the most straightforward method and requires no entity formation. You purchase the property in your personal name and hold the title directly.

Pros:

-

Simple transaction process

-

Fewer legal setup costs

-

No corporate maintenance obligations

Cons:

-

Full exposure to U.S. estate tax (only $60,000 exemption for non-residents)

-

Public ownership records (less privacy)

-

Limited asset protection

Most foreign buyers avoid personal ownership due to the estate tax risk alone.

Limited Liability Company (LLC)

A U.S.-based LLC is one of the most common ownership structures used by international buyers. It protects the identity of the owner and offers better estate planning options.

Pros:

-

Privacy (property held under company name)

-

Estate planning flexibility (transfer LLC interest instead of deed)

-

Limited personal liability

-

Centralized asset control

Cons:

-

Requires legal setup and annual maintenance

-

May be taxed differently depending on structure

-

Cannot be used in co-op buildings (which typically prohibit corporate owners)

An LLC is ideal for condo or townhouse purchases. You can establish the LLC in New York, Delaware, or Wyoming depending on your privacy and reporting preferences.

Trust Ownership

Some high-net-worth buyers use U.S. trusts or foreign irrevocable trusts to purchase real estate, especially when multi-generational planning is a priority.

Pros:

-

Estate planning control

-

Clear succession rules

-

Can avoid probate

Cons:

-

Complex legal and tax setup

-

Subject to trust taxation rules

-

Not ideal for short-term or investment purposes

Trusts are best suited for buyers planning to hold the property long-term and pass it on to heirs.

2. U.S. Income Tax and Withholding Rules

Owning U.S. property generates a range of tax responsibilities, even if you are not a U.S. resident. Understanding these rules upfront can help you avoid audits, penalties, or unnecessary double taxation.

Rental Income Taxation

If you rent your U.S. property, you must report that income to the IRS. The default rule is a flat 30 percent withholding on gross rental income. However, you can elect to be taxed on a net-income basis by filing Form W-8ECI and a U.S. tax return (Form 1040NR).

Withholding option:

-

Simpler but offers no deductions

-

No tax filing needed beyond annual 1042-S

Net income option:

-

Allows deductions (mortgage interest, property tax, maintenance)

-

Requires filing U.S. returns and keeping records

Many international investors opt for the net-income method to minimize their effective tax liability, particularly on long-term rental properties.

Capital Gains Tax

When you sell U.S. real estate, you may be subject to capital gains tax on the appreciation. Long-term gains are taxed at 15 to 20 percent for most non-residents, depending on the transaction structure.

Key factors:

-

Holding period (over one year qualifies for long-term rates)

-

Deductible costs (broker fees, closing costs, renovations)

-

State-level gains tax (New York has its own rate)

The FIRPTA Rule

The Foreign Investment in Real Property Tax Act (FIRPTA) requires buyers of U.S. real estate from foreign sellers to withhold 15 percent of the gross sale price at closing. This amount is sent to the IRS to cover potential capital gains tax.

Important points:

-

FIRPTA is a withholding tax, not the final tax owed

-

You can apply for a refund or reduced withholding (Form 8288-B)

-

A valid Individual Taxpayer Identification Number (ITIN) is required

FIRPTA applies regardless of your profit or loss on the sale. Planning your exit strategy early can help minimize this impact.

3. U.S. Estate and Gift Tax Exposure

Unlike citizens or permanent residents, foreign buyers are not entitled to the same estate tax exemptions. U.S. property is considered U.S.-situs property and falls under IRS estate tax rules.

Estate Tax Threshold

-

U.S. citizens: Exempt up to $13.61 million (2025 limit)

-

Non-resident aliens: Exempt only up to $60,000 in total U.S. assets

If a foreign owner dies holding U.S. property in their own name, their estate could face a tax of up to 40 percent on the property’s value above $60,000. This rule applies even if the owner resides outside the U.S. and holds neither a visa nor a green card.

Planning Solutions

To avoid or reduce estate tax exposure, foreign buyers often:

-

Hold the property through a U.S. LLC (with additional planning to avoid U.S. estate inclusion)

-

Use foreign blocker corporations or trusts (may complicate income tax reporting)

-

Purchase life insurance to cover the anticipated estate tax liability

-

Gift property interests during lifetime within legal limits

Proper structuring can significantly reduce or eliminate this liability, especially for family trusts or multi-property portfolios.

Gift Tax Rules

Gifting U.S. real estate interests also triggers different rules depending on the recipient's citizenship and the owner's residency. Foreign individuals cannot claim the same gift tax exemptions and must carefully structure any intra-family transfers.

4. Financing Challenges for Non-U.S. Buyers

Obtaining a mortgage in the U.S. as a foreign buyer is possible, but the process is stricter, slower, and more expensive than for U.S. citizens. Lenders assess risk differently for non-resident investors.

Lender Requirements

Foreign buyers typically need to provide:

-

A valid passport or visa

-

Proof of foreign income and assets

-

Bank statements (6–12 months)

-

International credit references or U.S. bank accounts

-

A larger down payment (30 to 50 percent)

Some banks may also request a U.S.-based guarantor or establish escrow requirements for future payments.

Higher Interest Rates and Fees

International buyers can expect:

-

Mortgage rates 1 to 2 percent higher than domestic buyers

-

Additional underwriting fees

-

Foreign national loan products with shorter terms or balloon payments

That said, U.S. mortgage interest is tax-deductible against rental income, so financing may help reduce your tax bill while preserving liquidity.

Lender Types

Options include:

-

Major U.S. banks with international divisions (J.P. Morgan, Citi International)

-

Niche lenders offering foreign national loan programs

-

Private banks and mortgage brokers experienced with international underwriting

Approval timelines range from 45 to 90 days depending on complexity and document authentication.

5. State and Local Tax Considerations in New York

Buying real estate in NYC introduces additional layers of taxation. From closing costs to annual fees, these taxes affect your bottom line.

New York Transfer Taxes

-

State transfer tax: 0.4 percent of purchase price

-

NYC transfer tax: 1 percent on deals up to $500,000, and 1.425 percent above

-

Mansion Tax: Starts at 1 percent for properties over $1 million and increases up to 3.9 percent above $25 million

These are typically paid at closing and not deductible from income.

Real Property Taxes

Annual property taxes in New York vary based on property type, location, and assessed value. For condos, the owner pays directly. For co-ops, taxes are embedded in monthly maintenance fees.

Additional Costs for Foreign Owners

Foreign buyers in NYC may face:

-

Higher title insurance premiums if buying through an entity

-

Non-refundable building application fees

-

Additional CPA fees for cross-border tax filings

-

Costs of hiring U.S.-based registered agents for LLC compliance

Summary of Key Considerations

|

Topic |

What You Need to Know |

|

Ownership Structure |

LLCs and trusts help with privacy and estate tax mitigation |

|

Rental Income Tax |

Elect net income treatment to deduct expenses |

|

FIRPTA Withholding |

15 percent of gross sale price; plan ahead for refunds or reduction |

|

Estate and Gift Tax |

Foreigners get only a $60,000 exemption; planning is critical |

|

Mortgage Access |

Requires more documentation and larger down payments |

|

New York Taxes |

Include transfer, mansion, and property taxes at city and state levels |

Plan Ahead to Avoid Surprises

Buying real estate in New York as an international buyer requires more than just a good property search. It demands proactive legal, tax, and financial planning from the start.

If you're exploring the NYC market from abroad, take the time to:

-

Choose the right ownership entity

-

Hire an attorney familiar with foreign investor rules

-

Understand your income, capital gains, and estate tax exposure

-

Coordinate with a cross-border accountant to ensure treaty compliance

-

Evaluate financing options early in the process

Each step you take toward planning will ultimately protect your capital, increase your return, and simplify your long-term ownership experience.